Tax liability in India is determined by the source and amount of income, place of receipt of income, and of course your residential status. As an NRI, you may have provisions for dual earnings – one in foreign currency from your investments or job in your country of residence or a third country and the other from your investment, rent, endorsements, etc. in India.

The current income tax law, applicable from 2020-21 onwards, says that if you are verified as an NRI, your income tax on foreign income received outside India will be totally free in India. However, your earnings in India will be taxable as per your income type and tax category.

Another point should be noted here if you receive your foreign income in India, it will be treated as your income generated in India and taxed accordingly.

However, resident Indians will have to pay tax on foreign income. So, if you are found to be a resident Indian, your income whether paid in a foreign country or in India will be taxable. Therefore, it is important for you to know the clauses that establish your tax status as an NRI and the new rules for NRIs in India.

Your residential status determines your tax status, which is broadly divided into two groups – Resident Indian and Non-Resident Indian.

Although they look to be two clearly defined groups, their definitions get altered from time to time in the book of the Income Tax department. That is done in order to curb the rate of tax evasion with fake NRI identities.

Let’s take a glance at the current version of definitions of Resident Indian and Non-Resident Indian.

You will be considered an NRI if

- your taxable income in India was more than 15 Lakh in an FY but you stayed in India for not more than 120 days in the same FY.

- your taxable income in India was less than 15 Lakh in a FY but you stayed in India for not more than 182 days in the same FY.

For all other conditions, a citizen of India will be considered a Resident Indian from a taxation point of view.

There is a subclause to the condition for NRIs that adds another layer of consideration. Even if your taxable income in India exceeded 15 lakhs in a fiscal year and you stayed in India for 120 days or more during the same fiscal year, the income tax department will conduct further checks. Specifically, they will assess whether your total stay in India over the last four fiscal years amounted to 365 days or more. If this criterion is met, you will be considered a resident Indian for tax purposes.

For those interested in gaining expertise in tax-related matters such as GST and income tax, consider enrolling in courses offered by GGC’s Practical Training Academy (GGCPTA). GGCPTA provides comprehensive GST and income tax courses. With practical insights and guidance from experienced professionals, these courses equip learners with the knowledge and skills needed to navigate the complexities of tax regulations effectively. Take your first step towards mastering tax-related topics by enrolling in GGCPTA’s GST and income tax courses today!

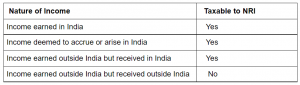

The below table provides NRI Tax liabilities considering the source of income and place of receipt of income.

.%20a%20href=https://ggcpta.com/GGCPTA/a%20provides%20comprehensive%20a%20href=https://ggcpta.com/products/accounting-taxation-course GST%20and%20income%20tax courses/a.%20With%20practical%20insights%20and%20guidance%20from%20experienced%20professionals,%20these%20courses%20equip%20learners%20with%20the%20knowledge%20and%20skills%20needed%20to%20navigate%20the%20complexities%20of%20tax%20regulations%20effectively.%20Take%20your%20first%20step%20towards%20mastering%20tax-related%20topics%20by%20enrolling%20in%20GGCPTA's%20GST%20and%20income%20tax%20courses%20today!span%20style=font-weight:%20400;The%20below%20table%20provides%20a%20href=https://virtualggc.com/service/nri-taxation-services/NRI%20Tax%20liabilities/a%20considering%20the%20source%20of%20income%20and%20place%20of%20receipt%20of%20income./spanimg%20class=aligncenter%20wp-image-6577%20src=https://virtualggc.com/wp-content/uploads/2021/12/Screenshot-38-300x85.png%20alt=Rules%20of%20Income%20Tax%20for%20Indian%20NRI%20Earning%20in%20Abroad%20Table%20width=708%20height=200%20/){kind=link}